Poultry Market Outlook - April

Discover the latest insights with our Poultry Market Outlook this month!

Stay ahead of the curve with up-to-date information on global poultry protein market prices.

Dive into our expert analysis and discover the driving forces behind the industry’s evolution.

Stay informed, stay ahead—don’t miss out!

FARM INPUTS PRICES – WORLDWIDE

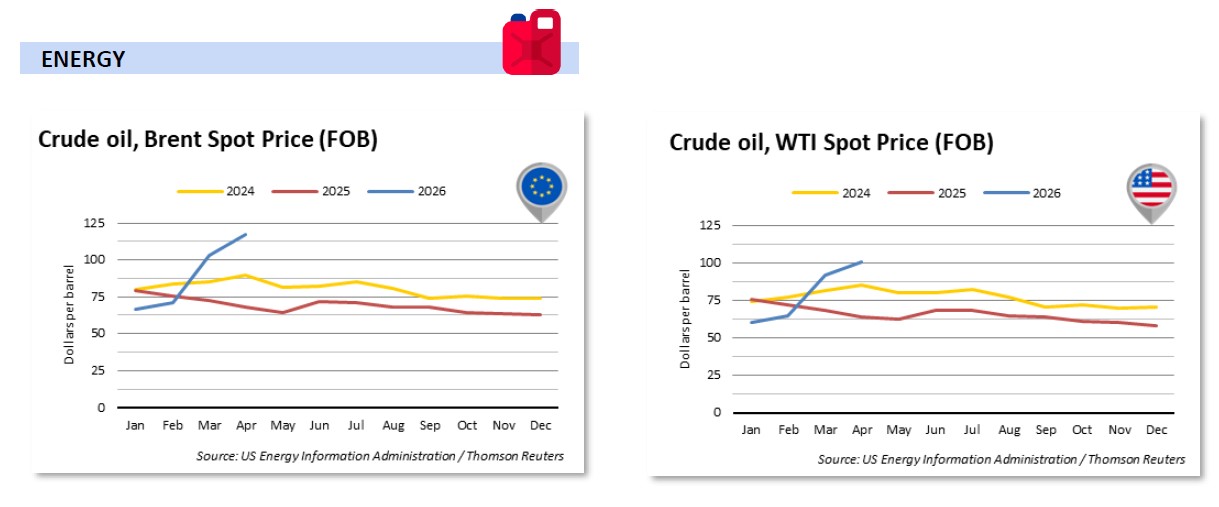

In April, commodity markets were influenced by both geopolitical and weather-related factors. Although volatility eased compared with March, tensions in the Middle East persist and continue to support energy and input prices.

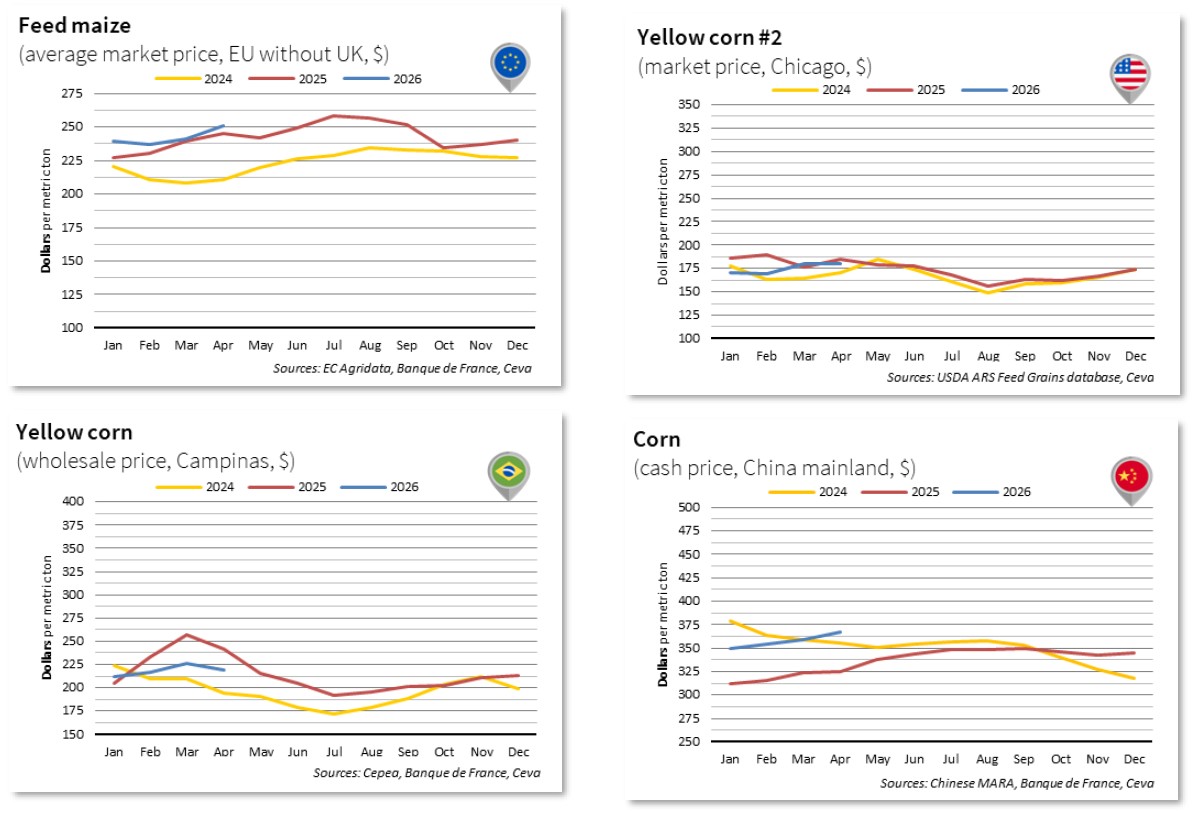

Corn

- On the European market, prices rose sharply over one month (+$10.4/t), reaching their highest level since September 2025. Uncertainty over the coming harvest, in this inflationary environment, is supporting prices.

- In Brazil, prices recorded their first real decline in nine months, falling to $219.1/t, compared with $225.8/t in March. Harvesting is progressing at a good pace and expected volumes are very strong (139.0 Mt, compared with a five-year average of 128.6 Mt).

- On the US market, corn prices stabilised at $179.9/t, compared with $179.5/t in March. Faced with rising production costs for this input-intensive crop, growers may revise their planting plans and shift some acreage in favour of soyabeans.

- China has not been spared by the rise in prices. Corn traded at $367.2/t on the Chinese market in April, a level not seen since January 2024.

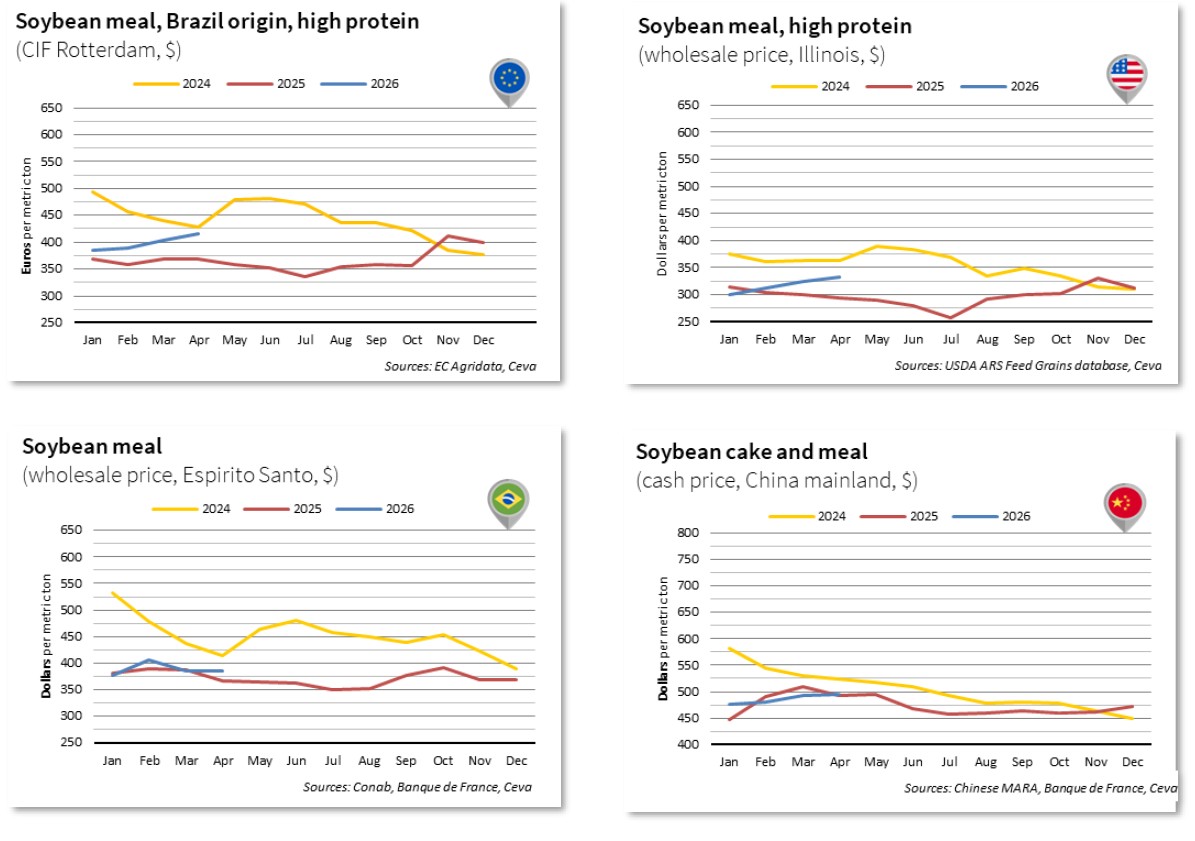

Soya and Soybean meal

- Unsurprisingly, prices on the European market, which is highly sensitive to global prices for this product, are following the US trend. Soyabean meal rose to $415.0/t in April, compared with $403.8/t in March.

- The soy complex continues its upward trend since autumn 2025: US soybean meal reached $333.3/t in April (+11.4% vs January), supported by higher oil prices and strong shipments to China.

- On the Chinese market, soybean meal prices rose modestly (+$2.5/t month-on-month), with future price trends largely dependent on the China–US trade agreement.

ENERGY

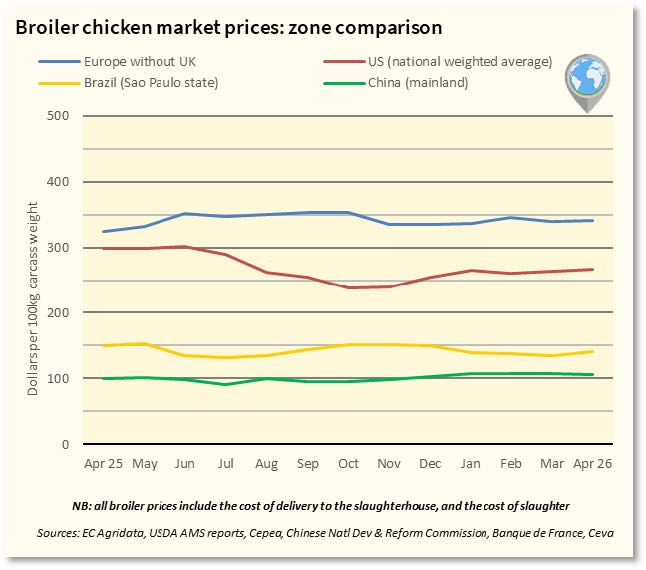

BROILER CHICKEN PRICE OVERVIEW – GLOBAL

European markets are easing in April, with live bird prices in Belgium and the Netherlands down around 10 cents/kg MoM. In Brazil, prices partially rebounded from March drop tied to Middle East trade disruptions. Input costs remain volatile with an upward bias, squeezing producers’ margins in surplus regions (notably Europe and China) where farmgate prices lag. Consumption growth stays positive, but conditions may weigh on H2 2026, making a supply-side correction increasingly likely.

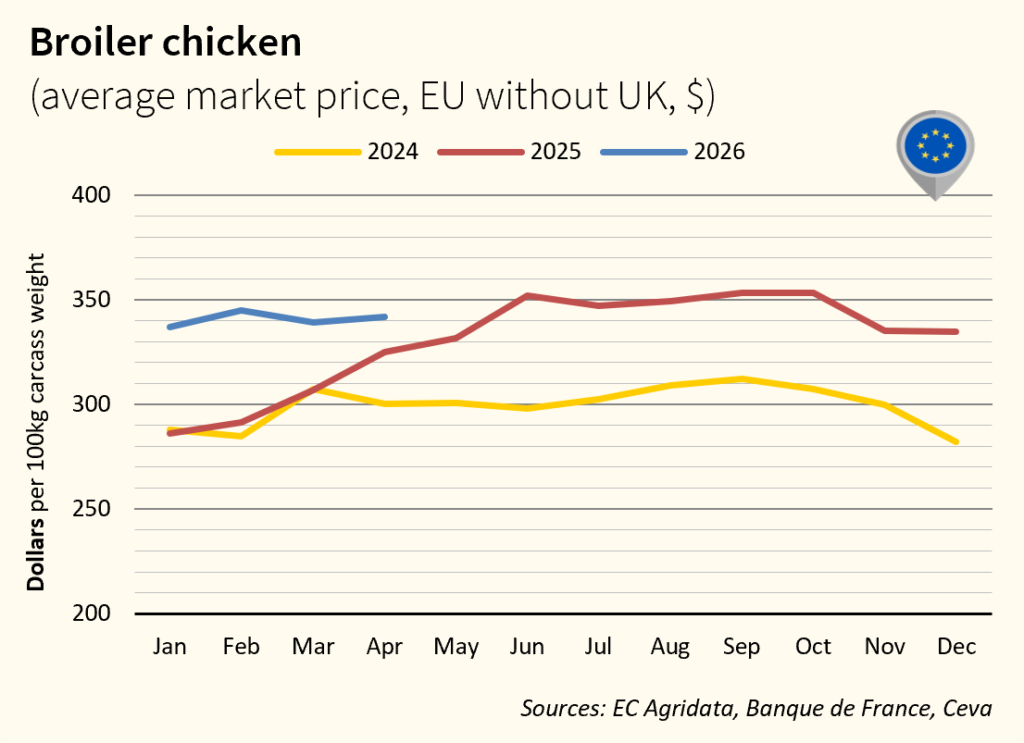

OVERVIEW – EUROPE

OVERVIEW – EUROPE

European chicken prices dipped 0.6% in April. The apparent increase on the chart is linked to a drop in the EUR-USD exchange rate. Live bird prices fell more sharply, with Deinze and ABC down over 10 cents/kg in a month (~‑10%). After months of tight supply, the market turned as Polish supply rebounded and Belgian/Dutch output surged. Low prices are expected for at least the next 10 weeks. Import pressure intensified the decline, with EU imports up ~100% YoY in April (Brazil +138%, Ukraine +121%, Thailand +78%).

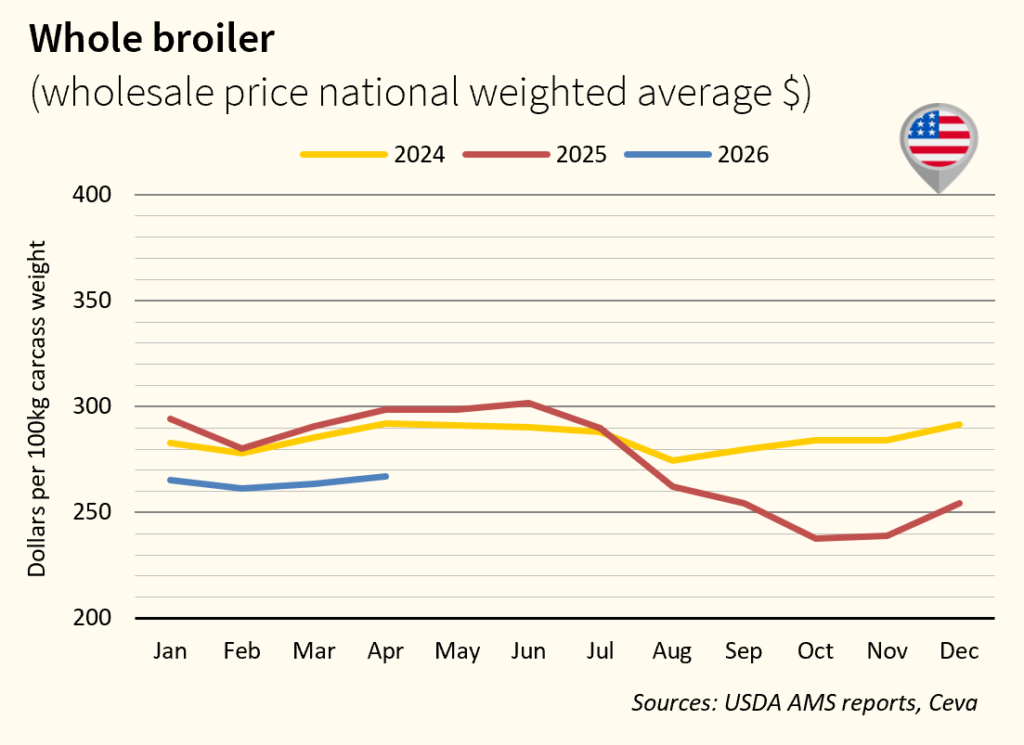

BROILER CHICKEN PRICE OVERVIEW – USA

US chicken prices edged up 1.3% in April. Market activity is described as moderate, with stable demand for whole birds and most cuts, while breast meat supply remains at least adequate. Dark meat – thighs and drumsticks – continues to see subdued activity. The market remains in an oversupply position, and hatchery data points to further pressure ahead: chick placements rose 3% in April year-on-year, suggesting the market will remain well-supplied in coming months. Prices are expected to stabilise or soften, in line with typical seasonal patterns

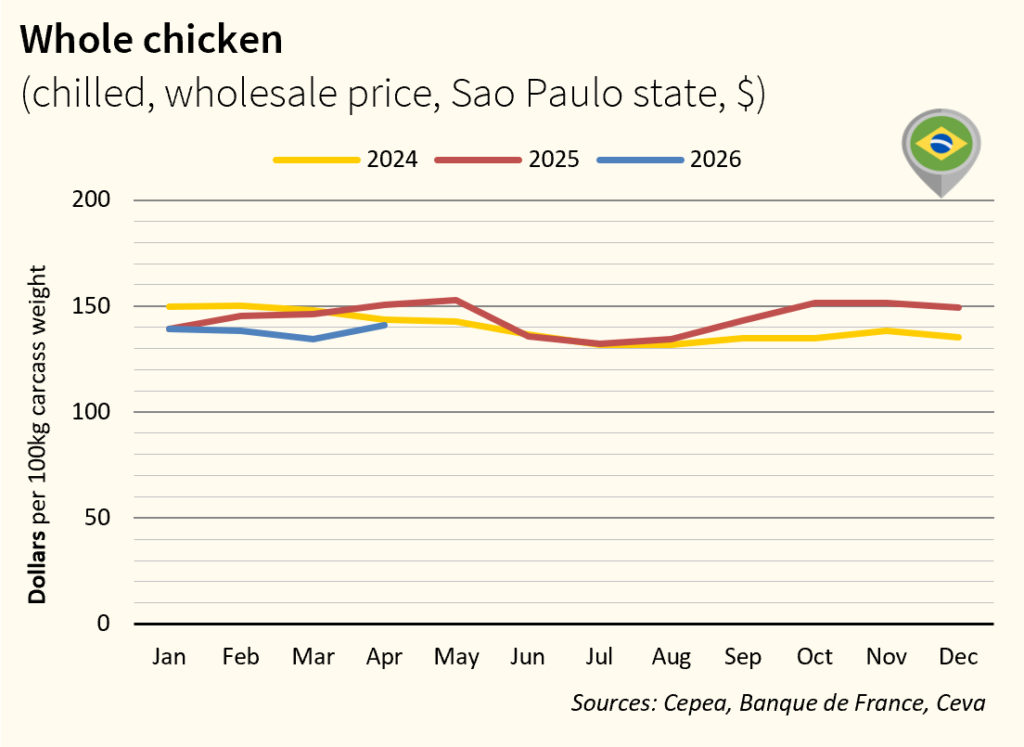

BROILER CHICKEN PRICE OVERVIEW – BRAZIL

Brazil’s chicken prices recovered in April on record exports and improved competitiveness. Volumes previously destined for the Middle East, were redirected to the EU, Africa and the Americas. April exports rose 3% YoY (record), despite the sharp drop in Middle East shipments (-24%), offset by Africa +37%, Europe +26% and the Americas +37%. Rising feed and energy costs continue to pressure producer margins despite firmer export prices.

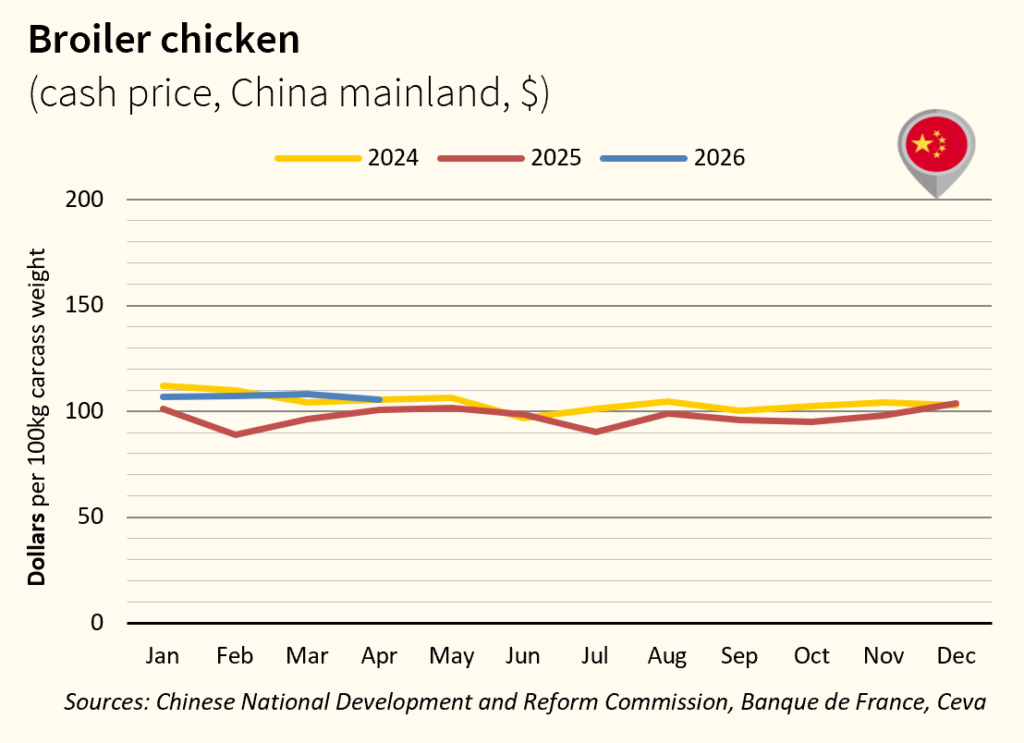

BROILER CHICKEN PRICE OVERVIEW – CHINA

In April, farmgate broiler prices in China edged slightly higher, improving farm-level profitability after several difficult months. While wholesale chicken prices remained under pressure – partly due to substitution from low pork prices – operators report a more dynamic market tone and a return to profitability. A growing number of processors are positioning on export markets as a structural growth driver and a market stabilisation lever. China exported approximately 150,000 tonnes of poultry in April, a record high and up 65% YoY.